AMD | Q1 2026: Share price rises 16% after another strong quarter

Advanced Micro Devices has started 2026 with a very strong quarter, confirming its emergence as a key player in artificial intelligence. The results show not only strong revenue growth, but above all a fundamental transformation in the structure of the business - the main driver is no longer personal computers, but data centers and AI infrastructure.

However, the first quarter also suggests that rapid expansion is not without costs. Although AMD is significantly increasing profits year-on-year, there is a slight retreat from record levels compared to the previous quarter. As a result, the company is now balancing between aggressive growth and maintaining profitability, which will be a key theme for investors in the months ahead.

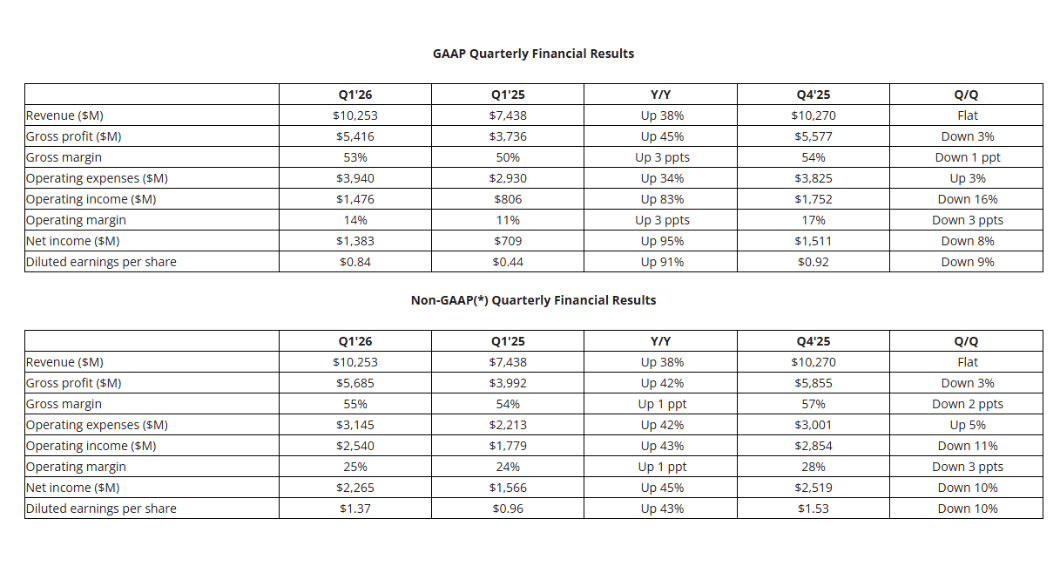

Revenues up 38%, profit almost double

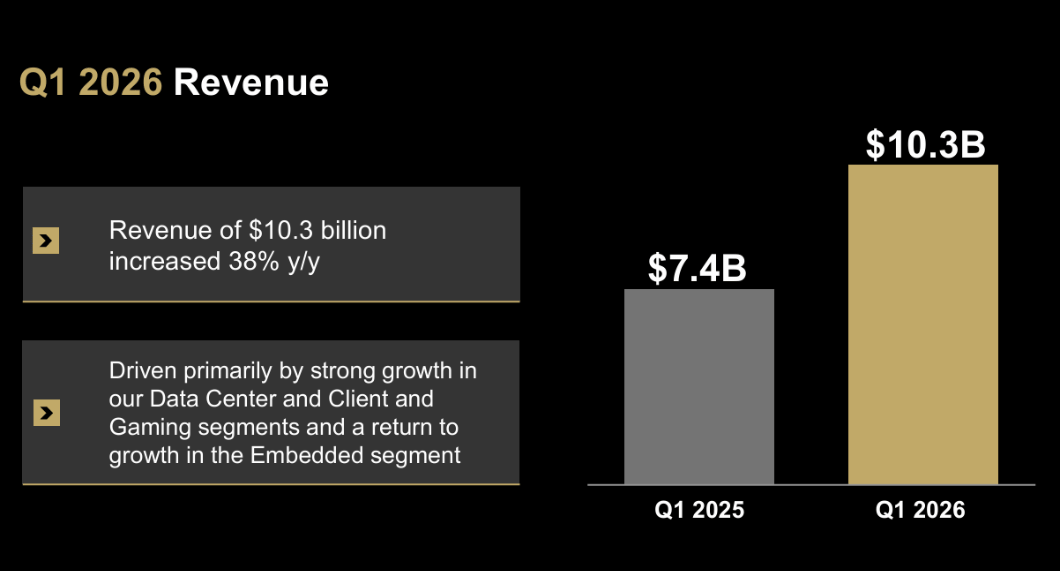

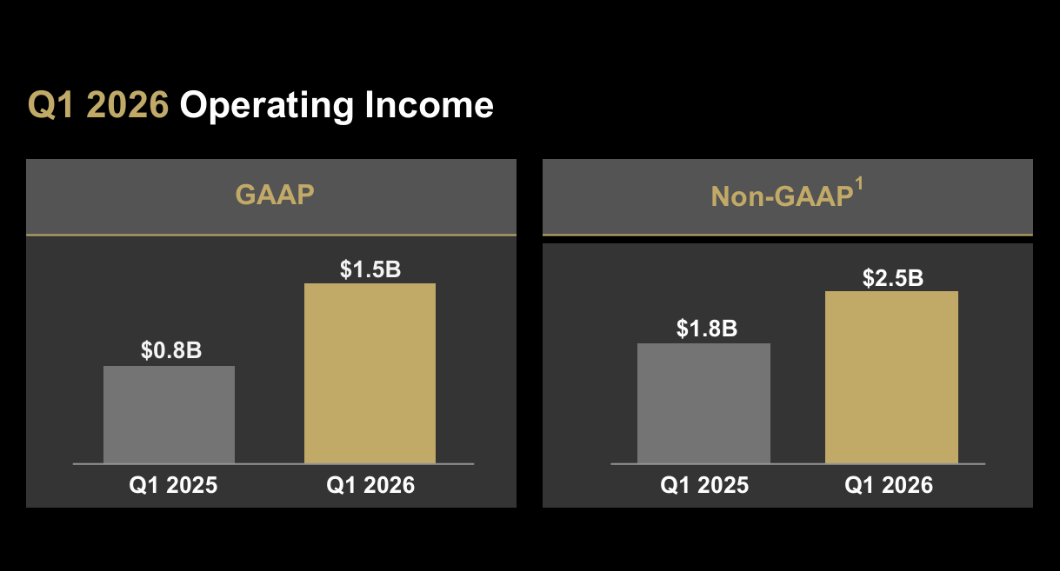

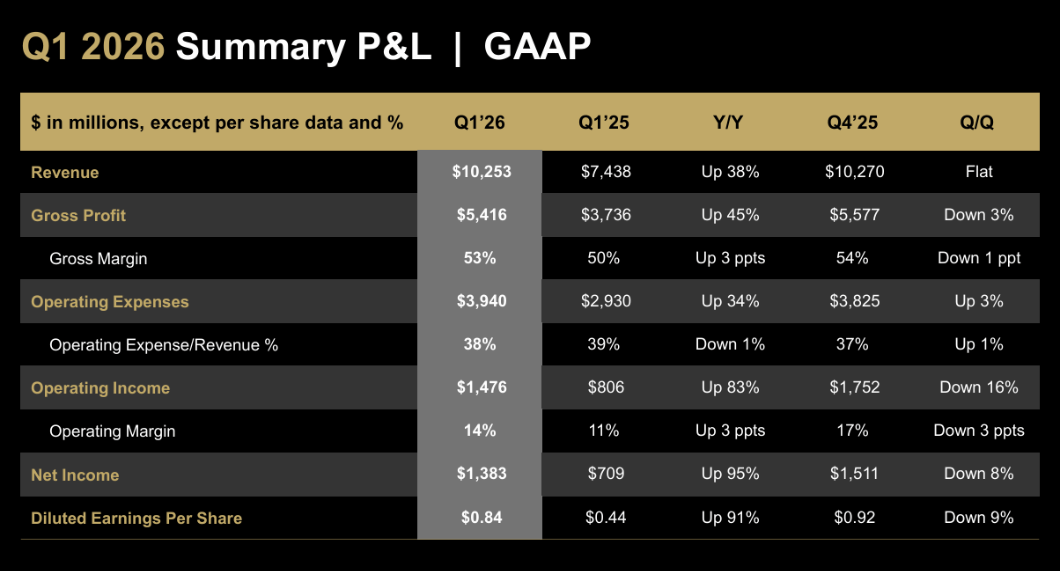

AMD $AMD reported first-quarter revenue of $10.25 billion, up 38% year-over-year. We see even stronger momentum in profitability, with net profit reaching $1.38 billion, up 95% year-over-year. Earnings per share rose from $0.44 to $0.84.

On an adjusted basis, earnings per share reached $1.37, up 43% year-over-year.

Data centres take the lead

Data centres are clearly becoming the most important segment. Revenues here reached $5.8 billion, up 57% year-on-year. This segment is now generating most of the company's growth and is gradually becoming the main source of profits.

This development is driven by strong demand for EPYC server processors and, in particular, Instinct AI accelerators. CEO Lisa Su pointed out that the demand for AI infrastructure continues to accelerate, mainly due to the development of inferencing and new types of AI applications.

The growing number of large customers is also very important. Collaborations with companies such as Meta, Microsoft, Google and Amazon confirm that AMD is gaining ground in cloud infrastructure. For example, Meta plans to deploy AI infrastructure of up to 6 gigawatts based on AMD chips.

PC segment revives, gaming remains mixed

Positive news is also coming from the client segment. PC processor sales rose 26% to $2.9 billion, indicating a market recovery and continued market share gains.

The gaming segment grew 11% to $720 million, but its development is less convincing. The growth in Radeon graphics card sales is partly offset by weaker results in custom chips, such as those for gaming consoles.

The Embedded segment then added 6% and remains a stable, if less dynamic, pillar of the company.

Higher costs as a tax for growth

One of the most important aspects of the results is the significant increase in costs. Operating expenses were up 34% year-over-year (on a GAAP basis), or 42% on an adjusted basis. This is the main reason why margins are down quarter-on-quarter.

CFO Jean Hu comments on this development as a result of investment in future growth. AMD is investing massively in new chip development, capacity expansion and building its AI ecosystem, which should be reflected in the coming years.

Strong outlook suggests further acceleration

The outlook for the second quarter is very optimistic. AMD expects revenue of around $11.2 billion, which would imply year-on-year growth of around 46% and quarter-on-quarter improvement of 9%. Gross margin should increase to around 56%.

This outlook confirms that demand for AI solutions remains very strong and that AMD will continue to benefit from the growing infrastructure investments of the tech giants.

AMD is building a complete AI ecosystem

In addition to the results themselves, the company announced a number of strategic moves. These include new generations of AI accelerators, collaborating with Samsung to develop advanced memory, and expanding the range of processors for servers and PCs.

Project Helios and a broader effort to build comprehensive AI solutions - from data centers to endpoint devices - are also interesting directions. AMD is thus not just trying to compete on the performance of individual chips, but on the entire ecosystem.

CEO comment

Lisa Su: "We delivered a great first quarter driven by accelerating demand for AI infrastructure. Data Centers are now a major driver of revenue and profit growth," says Lisa Su. "We see strong momentum in inferencing and AI agents driving demand for powerful CPUs and accelerators. Server growth will accelerate significantly as we scale delivery. Customer estimates for MI450 and Helios are exceeding our initial expectations and the pipeline of large deployments gives us better visibility into the future."

News and partnerships

Meta: up to 6 GW Instinct GPUs (first 1 GW on MI450), lead customer for 6th Gen EPYC "Venice/Verano"

Cloud hyperscalers: AWS, Google Cloud H4D, Azure, Tencent - new EPYC instances

MLPerf: MI355X leadership in inferencing

EPYC 8005: telco/edge optimization

Helios rack-scale AI: with TCS for India, NAVER/Upstage for Korea

Samsung: HBM4 for MI455X, DRAM for EPYC

Client: Ryzen AI PRO 400, Ryzen 9950X3D2 Dual Edition

Embedded: Ryzen AI P100, Kintex UltraScale+ Gen 2 FPGA

Omenjene delnice

Ta članek je bil napisan in pregledan v skladu z uredniškimi standardi Bulios.

Spremljajte Bulios na Google Novicah

Bodite med prvimi, ki izveste za nove analize, novice in premike na trgih.

Priporočeni članki

BLACK

BLACK BLACK

BLACK